Focus on the Family told the IRS in 2016 that it needed to be recognized as a church in order to avoid the Affordable Care Act’s mandate on insurance coverage for contraception and other regulations, according to documents that we have obtained from the IRS.

We reported in February that Focus on the Family, the influential Religious Right organization founded by James Dobson, is now classified as a church by the IRS, meaning that it does not have to file publicly available tax documents like most nonprofits do. In response to our request, the IRS sent us copies of its correspondence with Focus about the change in its status.

Those documents reveal that the IRS was initially skeptical of Focus’ claims but gave in after Focus’ lawyers insisted that the organization meets most of the tax agency’s criteria for houses of worship and that even questioning their status as a church could violate the First Amendment.

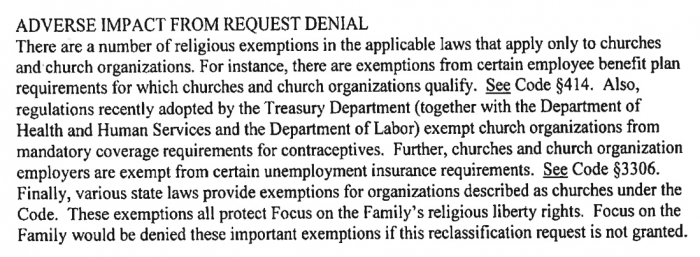

In May 2016, Focus wrote to the IRS requesting reclassification as a church, claiming that for “its entire existence, Focus on the Family has been a religious tax-exempt organization with many of the essential elements of a church.” It warned of the “adverse impact” it would face if the request was denied, namely that it would not be able to take advantage of “a number of religious exemptions” in law that “apply only to churches and church organizations.”

Focus specifically cited the Affordable Care Act’s contraception mandate, to which the Obama administration initially had carved out an exception for churches. The administration later allowed nonprofit religious organizations to opt out of the requirement and the Supreme Court’s 2014 Hobby Lobby decision expanded opt-out eligibility to include some for-profit corporations.

In becoming a church, Focus would also be exempt from some retirement plan regulations that apply to most nonprofits, and would no longer have to pay unemployment taxes or provide unemployment benefits to any employees who are fired. As we previously reported, churches are also exempt from filing publicly available tax documents with the IRS and are largely protected from audits.

In its letter to the IRS, Focus included a copy of its “moral behavior standards” for employees. Grounds for discipline include “non-biblical divorce,” “homosexual acts,” “transgender identity or expression” and “the use of Abortifacients”—a policy on the organization’s website says that it considers some methods of birth control, such as IUDs, to be abortifacients.

In August 2016, the IRS wrote back to Focus asking for more information, noting that the description of itself that the group had provided did “not appear to line up very strongly” with the list of 14 characteristics that the IRS considers in determining whether an organization is a church for tax purposes. Those characteristics include things like a “distinct ecclesiastical government” and “regular religious services.”

Gail Harmon, a tax attorney specializing in nonprofit law, told us via email that the IRS has a reason for drawing a careful distinction between religious nonprofits and churches. “The tax law distinguishes between religious organizations and churches,” she said. “Focus on the Family may be a religious organization but to say that it is a church renders that distinction meaningless.” If organizations like Focus begin to claim the special legal exemptions that Congress has carved out for churches, she said, “suddenly these legislative exemptions would become much more pervasive than Congress ever intended.”

Focus’ attorneys at the prominent law firm Holland & Knight responded to the IRS the next month with a remarkable letter in which they argued that Focus “satisfies all or most” of the IRS’ list of church characteristics and repeatedly accused the IRS of violating the First Amendment’s Establishment Clause by daring to question the group’s right to the tax law carve-outs reserved for churches.

In the letter, the attorneys claimed that Focus’ 600 employees are both its “ministers” and the members of its “congregation” and that the organization’s “chapelteria”—a cafeteria that also hosts regular staff worship services—is its “place of worship.” The organization’s board of directors are its “elders.” It’s president, Jim Daly, is its “head deacon and elder.” Listeners to the organization’s radio programs are “an extension of its congregation.”

“Without question, Focus on the Family’s members’ daily work is worship,” the attorneys wrote. At another point, they said: “Focus on the Family believes that all of its members are ministers.”

To the IRS’ statement that “there appears to be nothing distinctive” about the organization that “would cause a group of believers to coalesce around” it, the attorneys pointed to the “great number of pilgrims” who visit the organization’s Colorado Springs headquarters and the “wait list that Focus on the Family has for employment.”

The attorneys combed through the history of Christianity to find parallels between Focus and entities more commonly recognized as churches. They noted that John Wesley, the founder of Methodism, started out by founding a “Holy Club” whose members were associated with other churches before forming something that more closely resembled the established idea of a church. “So it is that as Focus on the Family continues to institutionalize, this church also is beginning to resemble others, subject to Focus on the Family’s own distinctive approach and messaging,” they wrote.

In response to the IRS’ pointing out that Focus doesn’t have Sunday services because its employees are worshiping at their home churches, the attorneys wrote that “Focus on the Family does not hold services on Sunday, but neither do many other churches such as the Seventh Day Adventists.” To the IRS’ comment that Focus’ “provisions for ecclesiastical governance are completely unlike those made by churches generally,” they noted that the Quakers have “long rejected altogether ordination for ministers.”

In response to the IRS’ comment that it “may question” the church status of an organization that, like Focus, “conducts excessive broadcasting or publishing,” the attorneys wrote that the organization’s media efforts have a biblical precedent: “Matthew and Mark record that Jesus got into a boat and went out a little ways to speak to crowds on the shore. Many biblical scholars think this is because of the amplification properties of water.”

To the IRS’ comment that the group’s “congregational/associational activities appear to be incidental to [its] media activities,” they wrote, “The notion that a ‘church’ is simply a building where people gather to hear a sermon every Sunday is not only antiquated, but also inconsistent with the description of the church found in the New Testament.”

Anthea Butler, a professor of religious studies at the University of Pennsylvania, looked over the correspondence and said that “a large part of what I’m seeing in this document about being a church has nothing to do with being a church.”

“A church is basically a pastor, with pastoral staff and members,” she said. “They don’t have that. They have employees.” She pointed out that one consequence of Focus’ contention that all of their employees are ministers is that they could take advantage of a federal law allowing ministers to deduct housing allowances from their income taxes.

Butler warned that under Focus’ interpretation of the law, “any nonprofit organization can be a church.”

“Everybody’s going to try to call themselves a church now,” she said.

On September 27, 2016, the IRS accepted Focus on the Family’s request.

Read the documents here:

- Full correspondence between Focus on the Family and the IRS

- Focus on the Family’s May 31, 2016 letter to the IRS requesting church status (Note: There are four pages missing from this letter, which we have requested from the IRS.)

- Focus on the Family’s September 8, 2016 response to questions from the IRS